1. INTRODUCTION

Like many jurisdictions worldwide, Alberta’s electricity system is undergoing considerable changes as its generation resource mix evolves. Between 2015 and 2024, the province saw a rapid decline in coal generation from meeting 50 per cent of total output to just 2 per cent, while renewable generation in the form of wind and solar has more than tripled as a share of output supplying 17 per cent of the market. The remainder of the market is served largely by natural gas generation, making up 78 per cent of generation in 2024.[1] With these changes comes new pressures on Alberta’s electricity market design which has remained relatively unchanged in its core elements since its inception in 2001.

This article outlines several key elements of ongoing market reforms in Alberta, referred to as Alberta’s Restructured Energy Market (“REM”). The REM was initiated in early 2024, with the Alberta Electric System Operator (“AESO”), the organization in charge of planning and operating Alberta’s electricity system, submitting a report on market reform recommendations.[2] After stakeholder engagement, the final REM proposal was released in August 2025, providing a clearer picture of the future direction of Alberta’s market design.[3] Throughout this process, the REM reforms were paired down in key ways from the original recommendations. The proposed REM adopts a number of important market reforms, but it maintains several unique features of Alberta’s relatively simplistic market design. While it could be argued that Alberta’s market has functioned well in the past and the simplicity is a feature not a bug, the changing technology mix and anticipated demand growth place distinct pressures on the prevailing market framework.

The growing pains facing Alberta’s electricity market are not unique. Many jurisdictions worldwide have adopted sophisticated market elements to deal with both the short-run and long-run challenges arising from the broader energy transition to increased renewable generation. This article draws from the considerable experience and empirical evidence from jurisdictions worldwide to highlight several key trade-offs being made in Alberta’s latest REM design proposal.

2. ALBERTA’S MARKET DESIGN AND GROWING CHALLENGES

Alberta’s electricity sector relies on market-based mechanisms having restructured its electricity market in 2001 from a setting with vertically integrated regional monopolies. While this is only one of two jurisdictions in Canada with a restructured market, the other being Ontario, there are numerous regions worldwide with restructured electricity markets with a diverse array of institutional settings and design elements.

At a high-level, Alberta’s current wholesale energy market has a single hourly market where generators submit bids to supply electricity. The AESO takes these bids, stacks them from least-to-highest costs until there is sufficient supply to meet demand. The highest accepted bid sets the market-clearing (uniform) hourly price that applies across the entire province. These bids are limited to be between $0/MWh and $999.99/MWh, with a price-cap of $1,000/MWh that can arise during scarcity conditions.

Alberta’s market design is what is often referred to as an “energy-only” market. In this setting, generators in Alberta rely solely on revenues from wholesale energy (and ancillary service) markets to recoup their large fixed cost of investing in generation capacity.[4] As part of this market design, Alberta has taken a unique viewpoint on permitting firms to exercise unilateral market power in the form economic withholding. That is, beyond the price floor and cap, firms are generally not restricted in the bids they submit in the wholesale energy market, permitting bids in excess of short-run marginal cost. The idea behind this being that to the extent that there is short-run market power, this will be disciplined by the entry of new generation capacity in the long-run.[5]

Electricity is delivered on a transmission network with physical constraints and is governed by laws of physics that determine how power flows through the network. Despite this, the physical nature of the network is not directly accounted for in the wholesale market clearing that sets an Alberta-wide uniform price. Historically, transmission congestion has been minimal in Alberta due in large part to a government policy referred to as the “no congestion” policy that effectively requires infrastructure build-out to ensure there is no congestion in the long-run.[6]

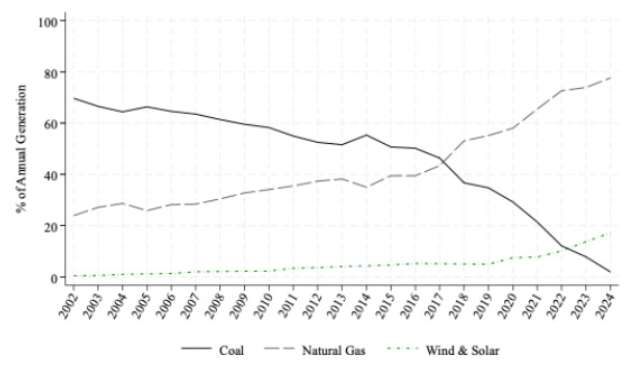

Figure 1 illustrates how Alberta’s generation mix has evolved since market restructuring in 2002 to 2024. The market has transitioned from a coal dominated market to being largely supplied by natural gas. While remaining a relatively small portion of the annual market share, wind and solar supplied 17 per cent of total output in 2024, representing a large increase over the last decade. This aggregate number masks important hourly dynamics that arise due to high wind and solar output resulting in an increasing frequency of supply surplus events, as well as higher fluctuations in net demand to be met by non-renewable generation.[7]

Figure 1: Annual Generation (% of Total) by Generation Technology[8]

The evolution of the market has introduced several pressing issues on the short-run operation of the system. First, while there is currently sufficient natural gas capacity in the province to meet demand, these units have to be turned on and ready to generate. A subset of gas generators incur large start up costs in addition to the variable cost of supplying output and can take up several hours to a full day to turn on. For these units, referred to as long-lead time (“LLT”) assets, it is generally not profitable to run all the time, leading their operators to have to make the economic decision of whether to start up the units in a setting with considerable uncertainty. This self-commitment mechanism has led to rising concerns over short-run reliability due to LLT units being offline in tight market conditions, an issue flagged by Alberta’s Market Surveillance Administrator (“MSA”).[9]

Second, the growth in geographically concentrated renewables has put increasing pressure on transmission infrastructure leading to increasing congestion.[10] Alberta’s wholesale energy market applies a single real-time price that ignores the presence of congestion. Congestion is dealt with via a secondary re-dispatch process that adjusts the supply of units to solve the transmission constraints and compensates them out-of-market. These re-dispatch mechanisms have been heavily criticized in the literature because of firms’ abilities to exercise market power and distort wholesale market outcomes.[11]

Alberta’s system planner (the AESO) is required to ensure the transmission system is subject to “no congestion” in the long-run. Without policy changes, this would require further build out of the transmission system to alleviate constraints. Transmission costs are passed down to consumers and have risen rapidly in the past decade. This has led to considerable debate over the need to adjust the prevailing transmission planning policy in the province.[12]

Finally, as noted above, Alberta is unique in its explicit stance on unilateral market power execution via economic withholding and its connection to long-run resource adequacy. Starting in 2021, there was a rise in market concentration and documented increase in unilateral market power execution.[13] Recent evidence from the MSA has indicated that economic withholding has declined as more generation capacity has entered the market.[14] However, the recent rise in wholesale energy costs has led to a renewed debate over whether additional regulations are needed to limit market power execution. This persistent debate relates to the broader long-run resource adequacy conversation that evaluates whether wholesale and ancillary service markets provide sufficient short-run revenues to cover the large capital cost associated with generation investment.

Before discussing the proposed REM and interim reforms that have been put in place over the past two years, the next section summarizes one key approach taken in other jurisdictions to address the challenges facing Alberta.

3. INTEGRATED ELECTRICITY MARKET DESIGNS

Restructured markets in other jurisdictions have adopted sophisticated market designs to address the key challenges highlighted above. This section will focus on so-called integrated market designs that are broadly deployed in the United States. This market framework has evolved to consider the physical characteristics of transmission infrastructure and unit constraints through a sequence of markets.

Like Alberta, these jurisdictions started with simplified market designs that focused primarily on balancing aggregate market supply and demand with a single market-wide price, solving system constraints via secondary processes (such as Alberta’s re-dispatch mechanism) to ensure feasibility. However, over 20 years ago, these markets moved away from this market design to address several of the challenges that are currently creating frictions in Alberta’s electricity system. While these markets have a vast array of technical and regulatory details that vary by jurisdiction, this article will highlight two core common elements of integrated markets: (i) multi-market settlement with a financial day-ahead market (“DAM”) and physical real-time market (RTM) and (ii) locational marginal pricing (i.e., nodal pricing).[15]

Starting a day in advance of real-time delivery, there is a financial DAM where firms submit bids that represent their willingness to supply electricity at different points (i.e., nodes) on the grid.[16] This bidding process also permits generators to submit “complex bids” that include their costs of starting up. The system operator (the equivalent of the AESO), takes these bids and chooses units to minimize the as-bid costs to meet location-specific demand, while accounting for physical constraints of the transmission network and unit-specific capabilities. This results in a schedule where if there were no changes between the day-ahead and real-time, this schedule could physically deliver energy at the right locations to balance supply and demand.

However, in reality, market conditions change after the DAM (e.g., due to changes in renewable output, market demand, gas unit availability, etc.). To manage such deviations, the system operator runs a real-time market (“RTM”) where generators can submit bids that represent adjustments from their DAM schedule. The RTM is also cleared to account for physical characteristics of the grid and unit capabilities and constraints with a process called Security Constrained Economic Dispatch (“SCED”). Unlike the DAM, clearing the RTM comes with a physical commitment with dispatch instructions that if they are not followed, the firms are subject to costly penalties.

The DAM results in a schedule that represents a financial commitment to supply a certain level of output at a particular location on the network. Despite the fact that the DAM does not come with a physical commitment, there is an inherent financial incentive to follow the DAM schedule. If a firm underdelivers from its DAM schedule, they must buy back this quantity in the RTM. This exposes the firm to financial risk that can be considerable if RTM conditions are tight (resulting in a potentially very high RTM price). Because of these strong financial incentives, and the fact that the DAM schedule is feasible by construction, most DAM bids go on to physical delivery.[17]

By considering the physical constraints of the system, the DAM and RTM market-clearing processes result in location-specific prices for each node on the network. These prices reflect the as-bid cost of serving an additional MWh of energy at a specific location on the network. This design is referred to as nodal pricing or locational marginal pricing (LMP). When there is no transmission congestion, the cost of serving demand at any given node is the same across all nodes. It simply reflects the cost of serving an additional MWh of supply from the market-level supply curve. However, when there is congestion, prices can diverge across nodes on the network, capturing the cost of addressing congestion. In these designs, generators often face the local nodal price, while end-users face a regional (zonal) weighted average price. It is important to emphasize that this market design addresses congestion within the wholesale bidding and market dispatch process. As a result, it does not require a secondary mechanism that addresses congestion via re-dispatch processes that have been shown to create market distortions and inefficiencies, as noted above.

In addition, the presence of the DAM is expected to facilitate more efficient pre-scheduling and unit commitment of long-lead time (“LLT”) units. Units that clear the DAM secure prices in advance, and in the case of LLT units in Alberta, they do not face the same challenge of turning on the unit and hoping they will end up being able to cover their start up costs in the RTM.[18] Facilitating financial hedging opportunities in the DAM in advance of the more volatile RTM is a broader benefit of multi-settlement market designs outside of just LLT units.

There is a growing literature documenting the benefits of integrated multi-settlement market designs with LMPs. A series of studies demonstrate that a transition from a simplified to integrated market design results in sizable economic improvements in short-run operational efficiencies.[19] Recent studies document evidence of increasing challenges in the presence of simplified market designs with increasing renewable generation, suggesting that the benefits of integrated market designs may be increasing.[20]

We would be remiss if we did not note the challenges of integrated market designs. First and foremost, they are complex, involve a multitude of regulations and rules, and require costly upgrades to software used to clear wholesale electricity markets. The literature has documented additional, more technical challenges that we will just briefly acknowledge, including slower responses to changing market conditions and reduced and difficulty of financial hedging when facing differential pricing at individual nodes on the network.[21] However, taken as a whole, the literature suggests that integrated market designs lead to more efficient short-run market outcomes and help alleviate the challenges of integrating often geographically concentrated renewable generation.

4. ALBERTA’S INTERIM REFORMS AND PROPOSED REM DESIGN

Now that we have an understanding of how Alberta’s market has evolved, the challenges it faces, and approaches used in other jurisdictions to mitigate these issues, we turn our attention to the ongoing and proposed market reforms in Alberta.

In March 2024, the Alberta government instituted the Supply Cushion Regulation to address concerns that LLT units were raising short-run reliability concerns by not turning on under tight supply conditions.[22] The approach outlined in the regulation was a non-market mechanism that turned on LLT units via an administrative approach that was triggered when market conditions were forecasted to be sufficiently tight. This was pitched as an interim measure to address reliability concerns until a broader market reform process was carried out.[23]

In January 2024, the AESO published initial recommendations on broader market reforms.[24] The recommended reforms were echoed in a direction letter from the Government of Alberta’s Minister of Affordability and Utilities in July 2024.[25] The initially proposed high-level reforms were a fairly holistic market redesign with a proposal to adopt many of the features of a multi-settlement integrated market outlined above. Key components that were explicitly stated were: (i) the development of a multi-settlement market with a DAM followed by a RTM, (ii) a market-clearing approach that uses bids in the RTM to minimize the cost of meeting demand, while accounting for the physical realities of the grid and unit constraints (referred to above as SCED), and (iii) a policy decision to move away from the current “no congestion” policy. These reforms represented a large departure from the existing simplified market design.

The initial reform proposal was followed by a year-long stakeholder process. In August 2025, the AESO released their final proposal for the REM.[26] The final REM proposal formalized a transition to LMP with SCED-based optimization of as-bid costs in the RTM that is a core element of integrated market designs. This market design will be increasingly important as Alberta is anticipated to continue to have transmission congestion in the long-run due to the transition away from the “no congestion” policy. The move to market-based congestion management via the adoption of LMP will avoid the pitfalls and inefficiencies of secondary re-dispatch mechanisms outlined above.

However, one critical change from the initial proposal is that Alberta will not transition to a multi-settlement market design, i.e., there will be no financially binding day-ahead energy market.[27] Rather, the proposed REM sticks with a process similar to the interim approach outlined in the Supply Cushion Regulation. This process, now called the Reliability Unit Commitment (“RUC”), continues with the administrative approach of directing LLT units online when market conditions are forecasted to be sufficiently tight, with cost recovery guarantees.

The decision to not move forward with a day-ahead energy market reduces the complexity of the market design, an important trade-off to acknowledge. However, it differs from the trajectory taken in nearly every other restructured electricity market worldwide to manage the increasing challenges of integrating renewable generation. For example, the development of a multi-settlement DAM-RTM with LMPs has recently been finished in Ontario as part of its Market Renewal. The implementation of a financially binding DAM was noted as a key improvement in Ontario’s market design.[28]

The latest proposal for the REM moves Alberta towards a market design that is closer to that which has been employed for over 20 years in Singapore and New Zealand.[29] These market designs have single-settlement systems with RTMs and LMPs. Recent work in the context of New Zealand has highlighted the reliability challenges of this market design with increasing renewable generation.[30] This market design is an improvement on Alberta’s historical simplified market design, but it does not achieve several of the key benefits that come with DAMs, including a market-based mechanism to facilitate efficient “turn on” decisions of LLTs and an avenue for generators and the demand-side to hedge price risk in advance of the typically more volatile RTM.

To summarize, the proposed REM design includes several important market reforms, including the transition to LMP, more sophisticated optimization in the RTM to account for physical realities of the grid and generation technologies, and additional improvements to ancillary service markets that are beyond the scope of this article. However, the decision to not adopt a DAM comes with the trade-off of attempting to reduce the complexity of the market design with the well-documented benefits of multi-settlement DAM-RTM designs.

5. LONG-RUN RESOURCE ADEQUACY

Much of the discussion in this article has focused on the short-run operation of the market. However, a long-standing tension in Alberta, and any restructured market design more broadly, is designing a market that promotes sufficient generation capacity investment to ensure there is sufficient supply to meet demand at (nearly) all points in time. This is often referred to as promoting long-run resource adequacy. It is important to briefly highlight how the proposed REM interacts with these long-run objectives.[31]

In nearly every jurisdiction with restructured energy markets, there are limits on wholesale price-levels. In Alberta, the wholesale price cap is set at $1,000/MWh. The presence of these wholesale price caps has led to a long-standing debate over whether or not there will be sufficient generation capacity investment in restructured markets.[32]

As discussed in Section 2, Alberta’s market framework takes the unique stance that unilateral market power is an element of the market design. The market design permits a trade-off of short-run inefficiencies due to market power with long-run investment signals, i.e., in the long-run, entry is expected to discipline the market. There have been periods of considerable market power execution in Alberta when market conditions are tight, followed by capacity investment and reduced wholesale energy prices in Alberta.[33] Despite the challenges associated with this “boom-and-bust” cycle, Alberta’s market design has been successful in promoting sufficient capacity investment.

In 2024, after several years of elevated wholesale prices and high-levels of documented market power, the Government of Alberta adopted the Market Power Mitigation Regulation as an interim approach until broader reforms under the REM are put in place.[34] The regulation serves as a “safety valve” that evaluates if firms have earned excessive market power revenues beyond the levels that are deemed necessary to promote long-run capacity investment signals. Once generators are determined to have earned sufficient revenues, limits are placed on bids of gas generators owned by the large generators.

In the AESO’s final proposed REM design, this “safety value” interim approach will be a core part of the market design, with some adjustments to the details. In addition, the wholesale price cap will be increased to $3,000/MWh, closer to levels observed in other jurisdictions as a mechanism to better signal scarcity on the system to promote investment. Finally, there will be an offer cap (representing a ceiling on firms’ bids) of $1,500/MWh initially, followed by an increase to $2,000/MWh in 2032. Market-clearing prices (but not bids) can rise above the offer cap to the wholesale price cap through an administrative scarcity pricing mechanism that is triggered when the market dips into ancillary service markets because of limited supply in the wholesale market. Such administrative scarcity pricing approaches have been broadly deployed in US markets to enhance price signals during scarcity events.[35]

However, this scarcity-pricing plus market power approach differs from approaches taken in the majority of other jurisdictions. In particular, while the proposed REM now places more regulations on bidding to restrict what is deemed as excess market power, it is still considerably less restrictive than bid mitigation approaches in other jurisdictions.[36]

To alleviate concerns of resource adequacy, other jurisdictions (with more stringent regulations of market power) have adopted capacity payment mechanisms. These are separate markets that typically take place years in advance of the actual delivery of electricity and aim to fill the gap between the cost of capacity investment and the expected revenues from energy markets. However, there is a growing literature documenting the considerable issues with capacity mechanisms, including their high degree of complexity, costs of operating, heavy regulatory requirements, and poor fit with the growth of renewables.[37] Alberta considered adopting a capacity market in 2016. However, in 2019, the move to a capacity market was terminated.[38]

Alternatives to capacity markets that rely on longer-term financial forward contracting have gained some traction in ongoing policy debates.[39] Without getting too deep into the details, this approach essentially aims to facilitate longer-term risk-hedging opportunities that currently do not exist, with the idea of reducing hesitancy in undertaking large capital-intensive investments in generation capacity in a highly uncertain environment. However, the use of these more frontier mechanisms were not proposed in the REM.

The interim reforms and final REM proposal is taking a fairly status-quo approach to resource adequacy, with additional market design elements to strengthen energy market price signals and new regulatory tools to limit excessive market power execution. While Alberta’s market design has been successful in promoting resource adequacy under this design, there are questions of whether this approach will continue to be successful with the rising uncertainty and variability of energy prices that comes with the growth of renewable generation.

6. CONCLUSIONS

Facing a considerable transition in the generation resource mix, Alberta has undertaken market reforms to address growing challenges and cost pressures. The proposed reforms make several important changes to the prevailing market design, adopting key features that exist in other more sophisticated markets. However, the proposed REM remains anchored in several key market design elements that are particular to Alberta. While this helps maintain the simplicity of Alberta’s electricity market design, the more sophisticated, but complex, elements such as the use of multi-settlement DAM-RTMs come with their distinct advantages. Time will tell whether these decisions will lead to additional required market reforms in the future.

-

* David Brown is a Professor of Economics at the University of Alberta where he holds a Canada Research Chair in Energy Economics and Policy. He is a Faculty Affiliate at Stanford University’s Program on Energy and Sustainable Development. David has served as the president of the Canadian Association for Energy Economists since 2020. His expertise lies at the intersection of energy economics, industrial organization, and regulatory policy.

David Brown is engaged as a subcontractor for FTI Consulting on the ongoing AESO’s ISO Tariff Redesign project. The views and opinions expressed in this piece are solely his own and do not necessarily reflect those of FTI Consulting or its clients. David was not privy to any confidential or non-public information concerning the matters addressed in the article and has exclusively relied on publicly available information.

1 Alberta Utilities Commission, “Annual Electricity Data”, online: <auc.ab.ca/annual-electricity-data>.

-

2 Alberta Electric System Operator, “Alberta’s Restructured Energy Market: AESO Recommendation to the Minister of Affordability and Utilities” (31 January 2024) online (pdf): <aesoengage.aeso.ca/37884/widgets/156642/documents/125532>.

-

3 Alberta Electric System Operator, “Restructured Energy Market: Final Design” (August 2025), online (pdf): <aeso.ca/assets/REM/Restructured-Energy-Market-Final-Design.pdf>.

-

4 Ancillary service markets are supplemental markets that ensure supply and demand are balanced at all moments in time. While these markets are essential and are part of key reforms under the REM, they are out of the scope of the current article.

-

5 For a more detailed discussion on this point and broader market design elements, see Derek E. H. Olmstead & Matt J. Ayres, “Notes from a Small Market: The Energy-Only Market in Alberta” (2014) 27:4 Electricity J 102; See also David P. Brown et al., “Electricity Market Design with Increasing Renewable Generation: Lessons from Alberta” (2025) Electricity J 107484 [Lessons from Alberta].

-

6 For a detailed discussion of the history of transmission policy in Alberta, see Government of Alberta, “Transmission Policy Review: Delivering the electricity of Tomorrow” (23 October 2023), online (pdf): Ministry of Affordability and Utilities <ablawg.ca/wp-content/uploads/2023/11/Transmission-Policy-Green-Paper-2023.pdf>.

-

7 In 2024, the market-clearing price was $0.00/MWh due in part by high renewable output for 532 hours beating the previous record set in 2023 of 83 hours. See Alberta Market Surveillance Administrator, “Quarterly Report for Q4 2024” (February 2025) at 13, online (pdf): MSA <albertamsa.ca/assets/Documents/Quarterly-Report-for-Q4-2024.pdf>.

-

8 Figure recreated from Figure 1 in Lessons from Alberta, supra note 5.

-

9 See Alberta Market Surveillance Administrator, “Quarterly Report for Q2 2024” (August 2023) at 34, online (pdf): MSA <albertamsa.ca/assets/Documents/Quarterly-Report-for-Q2-2023.pdf>.

-

10 For a detailed discussion, see Alberta Market Surveillance Administrator, “Quarterly Report for Q1 2024” (May 2024) at 34, online (pdf): MSA <albertamsa.ca/assets/Documents/Quarterly-Report-for-Q2-2023.pdf>.

-

11 For a detailed analysis of this issue, see Christoph Graf et al., “Simplified Electricity Market Models with Significant Intermittent Renewable Capacity: Evidence from Italy” (2020) National Bureau of Economic Research, Working Paper No 27262, online (pdf): <nber.org/system/files/working_papers/w27262/w27262.pdf>.

-

12 Supra note 6.

-

13 David P. Brown et al., “Evaluating the Impact of Divestitures on Competition: Evidence from Alberta’s Wholesale Electricity Market” (2023) 89 Int’l J of Industrial Organization.

-

14 See Alberta Market Surveillance Administrator, “Wholesale Market Report: Q1 2025” (May 2025) at 24, online (pdf): MSA <albertamsa.ca/assets/Documents/Wholesale-Market-Report-Q1-2025.pdf>.

-

15 For a comprehensive comparison of simplified versus integrated market designs, see Christoph Graf, “Simplified Short-Term Electricity Market Designs: Evidence from Europe” (2025) Electricity J.

-

16 These markets also permit location-based demand-side bidding. However, for brevity, we abstract away from the demand-side in this article.

-

17 Udi Helman et al., Competitive Electricity Markets, Chapter 5: The Design of US Wholesale Energy and Ancillary Service Auction Markets: Theory and Practice (2007) 180.

-

18 In addition to securing a price in advance, LLT units that submit complex bids and clear the DAM secure a “revenue sufficiency guarantee” where if they do not earn enough revenue to cover their start up costs from operating, they are provided additional payments (called uplifts) to break even.

-

19 See Frank A. Wolak, “Measuring the Benefits of Greater Spatial Granularity in Short-Term Pricing in Wholesale Electricity Markets” (2011) Am Econ Rev; See also Jay Zarnikau et al., “Did the introduction of a nodal market structure impact wholesale electricity prices in the Texas (ERCOT) Market?” (2014) J of Regulatory Econ; See also Ryan C. Triolo & Frank A. Wolak, “Quantifying the Benefits of a Nodal Market Design in the Texas Electricity Market” (2022) 112:1 Energy Econ.

-

20 For example, see supra note 11.

-

21 Ahlqvist Victor et al, “A Survey Comparing Centralized and Decentralized Electricity Markets” (2022) Energy Strategy Rev.

-

22 See Supply Cushion Regulation, Alta Reg 42/2024.

-

23 For a detailed discussion of the interim market reforms running up to the REM proposal, see Alberta Market Surveillance Administrator, “Advice to support more effective competition in the electricity market: Interim action and an Enhanced Energy Market for Alberta” (December 2023), online (pdf): MSA <albertamsa.ca/assets/Documents/MSA-Advice-to-Minister.pdf>.

-

24 Alberta Electric System Operator, “Alberta’s Restructured Energy Market: AESO Recommendations to the Minister of Affordability and Utilities” (January 2025), online (pdf): <aesoengage.aeso.ca/37884/widgets/156642/documents/125518>.

-

25 See the letter from the Minister of Affordability and Utilities of Alberta, Nathan Neudrof, to the President and Chief Executive Officer of the Alberta Electric System Operator, Mike Law (3 July 2024), online (pdf): <aeso.ca/assets/direction-letters/Direction-Ltr-from-Minister_REM_Tariff_Tx-Policy_03July2024.pdf>.

-

26 Alberta Electric System Operator. Restructured Energy Market Final Design. August 2025. Alberta Electric System Operator, “Alberta’s Restructured Energy Market: Final Design” (August 2025), online (pdf): <aeso.ca/assets/REM/Restructured-Energy-Market-Final-Design.pdf>.

-

27 Ibid at 6, the AESO makes reference to a Day-Ahead Reliability Market. This is the same as a financially binding day-ahead energy market. While similar language, this reflects day-ahead ancillary service markets that are critical to maintaining short-run reliability.

-

28 Independent Electric System Operator, “Day-Ahead Market High-Level Design: Executive Summary” (August 2019).

-

29 For a detailed analysis of Singapore and New Zealand, see Frank A. Wolak, “An Assessment of the Performance of the New Zealand Wholesale Electricity Market” (2009) Stanford University Research Working Paper No 94305-6072, online (pdf): <fawolak.org/pdf/new_zealand_report_redacted.pdf>; See also Frank A. Wolak, “The Benefits of Purely Financial Participants for Wholesale and Retail Market Performance: Lessons for Long-Term Resource Adequacy Mechanism Design” (2019) 35:2 Oxford Rev of Econ Pol’y 260, online (pdf): <fawolak.org/pdf/oxford_economic_policy_pub_wolak.pdf>.

-

30 Shaun McRae, “Rethinking Wholesale Market Design for New Zealand’s Clean Energy Transition” (2025) Electricity J, online (pdf): <sdmcrae.com/files/rethinking-market-design.pdf>.

-

31 For a more detailed discussion on the issue of resource adequacy and Alberta’s market design, see Lessons from Alberta, supra note 5.

-

32 Frank A. Wolak, “Long-Term Resource Adequacy in Wholesale Electricity Markets with Significant Intermittent Renewables” (2022) 3:1 Envt and Energy Pol’y and the Econ 155, online (pdf): <journals.uchicago.edu/doi/epdf/10.1086/717221>.

-

33 Supra note 13.

-

34 Market Power Mitigation Regulation, Alta Reg 43/2024.

-

35 For a detailed discussion of this market design referred to as the Operating Reserve Demand Curve (ORDC) in the Texas context, see William W. Hogan and Susan L. Pope “Priorities for the Evolution of an Energy-Only Market Design in ERCOT” (May 2017) FTI Consulting, online (pdf): <hepg.hks.harvard.edu/sites/g/files/omnuum10586/files/hepg/files/hogan_pope_ercot_050917.pdf>.

-

36 Christoph Graf et al., “Market Power Mitigation Mechanisms for Wholesale Electricity Markets: Status Quo and Challenges” (2021) Stanford University, Working Paper, online (pdf): <web.stanford.edu/group/fwolak/cgi-bin/sites/default/files/MPM_Review_GPQW.pdf>.

-

37 For a more detailed discussion of capacity mechanisms, see Pär Holmberg & Tangerås Thomas, “A Survey of Capacity Mechanisms: Lessons for the Swedish Electricity Market” (2023) 44:6 Energy J 275; See also Lessons from Alberta, supra note 5.

-

38 Legislative Assembly of Alberta, Bill 18. Electricity Statues (Capacity Market Termination) Amendment Act, 2019. Bill 18, Electricity Statutes (Capacity Market Termination), 1st Sess, 30th Leg, Alberta, 2019.

-

39 Supra note 32.