1. MARKET RENEWAL ARRIVES IN ONTARIO

On May 1st, 2025, Ontario’s Independent Electricity System Operator (“IESO”) officially launched its renewed market, known as the Market Renewal Program ((“MRP”) or the “renewed market”). The renewed market represented the most significant redesign of the IESO-administered market (“IAM”) in Ontario since it was first introduced in 2002. While the renewed market resulted in hundreds or thousands of different changes to settlement systems, Market Rules and Market Manuals, there are a few overarching design components that were central to the overhaul of the renewed market.

-

- Locational Marginal Prices (“LMPs”)– The move to locational based pricing across the IAM eliminated what was known as the two-schedule market that played a significant role in the legacy market. By introducing a single schedule market and the resulting LMPs, prices now fully reflect transmission congestion and losses and more accurately reflect the true cost of consumption at different locations on the grid.

- Financially Binding Day-Ahead Market (“DAM”) – The DAM provides financially binding schedules for Market Participants (“MPs”) across the IAM and replaces the non-financially binding day-ahead commitment process that was in place in the legacy market. Most supply is now procured in the DAM.

- Enhanced Real-Time Unit Commitment (“ERUC”) – The IESO updated and refined its commitment programs for what are known as Non-Quick Start (“NQS”) generators, which are predominantly gas-fired generators. NQS resources typically require the dispatch algorithm to consider a number of operational and physical constraints. Under the ERUC changes, the financial and physical constraints of different NQS resources are intended to be more optimized and efficiently committed than occurred with the commitment programs in the legacy market.

- Market Power Mitigation (“MPM”) – The mitigation framework for all resources was moved from an ex post (“after the event”) clawback of out-of-market payments to an ex ante (“before the event”) screening of various financial and physical parameters.

The following sections provide a high-level overview of known flaws of the legacy market that prompted MRP before discussing outcomes in the renewed market over the first six months of operation. The discussion on the legacy market and its flaws will remain high-level, as most of these flaws have been discussed (and cited in footnotes) at length in multiple settings throughout the last two decades.

2. A BITTERSWEET SYMPHONY: THE LEGACY MARKET DISAPPEARS AND REMOVES PRICE SUPPRESSION MECHANISMS

The legacy market in Ontario had a number of well-understood and well-known deficiencies. In some cases, these deficiencies were intended to be addressed within a few years of the market being launched in 2002. For a variety of reasons, these deficiencies became embedded in the overall market design and were some of the most recognizable “features” of the Ontario wholesale market compared to a number of other wholesale markets across North America.

The IESO and the Market Surveillance Panel (“MSP”) highlighted many of the flaws of the legacy market throughout its more than 20 years in operation. The most comprehensive report on the flaws of the wholesale market was the MSP’s 2016 report “Congestion Payments in Ontario’s Wholesale Electricity Market: An Argument for Market Reform”. The IESO also provided a detailed review for a number of the deficiencies in the wholesale market as part of the evidentiary record in a Market Rule appeal by a group of NQS generators.[1]

The IESO also presented its “Energy Stream Business Case” for the Market Renewal Program, that included $975 million in savings over ten years, with $97.5 million in annual savings coming from the combination of the elimination of constrained off CMSC ($45 million/year) and market efficiencies ($52.5 million/year).[2] The market efficiencies benefits were summarized by the IESO as “more efficient use of interties (particularly exports), better unit commitment and enhanced competition will result in better asset utilization and reduced natural gas burn, avoiding fuel cost”.[3]

The most notable flaws and deficiencies of the legacy market are discussed below.

i. Legacy Market Prices Did Not Reflect Physical Limitations of the Grid (The Two-Schedule System)

The Two-Schedule System in the legacy market required two different algorithms to dispatch units and set wholesale prices. In the “dispatch” algorithm, the physical constraints of different units and the transmission grid were considered in order to physically dispatch the units and create a “dispatch schedule”. The “market” algorithm then created a “market schedule” that ignored the physical constraints of both Market Participants and the transmission grid to create a Market Clearing Price (“MCP”) that was uniform across the province and used for settlements. The market schedule was “fictional” in the sense that it did not account for how all the units were physically dispatched in the “dispatch” schedule and, as such, was not based on the actual cost and dispatch of the grid.

Divergences between the two schedules required out-of-market payments known as Congestion Management Settlement Credits (“CMSCs”), which resulted in both a number of “gaming” issues and overall economic inefficiencies, as detailed by the MSP throughout the last two decades.[4] It also blunted the reality that the cost of electricity consumption differed in various parts of the grid due to well-known transmission constraints — leading to both inefficient dispatch and consumption.

ii. Legacy Market Had Inefficient Commitment Programs for Gas (“NQS”) Generators

When the wholesale market launched in 2002, there were no commitment programs for NQS generators as they were expected to fully rely on spot energy prices for dispatch and operational revenues. Over time, the IESO developed both real-time and day-ahead commitment programs. The real-time program — known as the Real-Time Generator Cost Guarantee (“RT-GCG”) — committed NQS generators in the pre-dispatch timeframe based on their incremental energy costs only and did not consider other start-up-related costs. The RT-GCG program also did not account for commitment over multiple hours — even though most NQS generators must physically remain online for numerous consecutive hours — and that resulted in commitments that were “inefficient and disadvantageous to lower cost NQS resources.”[5]

Under the legacy market, many NQS generators could self-commit themselves under an RT-GCG program that did not incorporate system-wide conditions when committing long-lead time resources. Instead, NQS generators could self-commit their units when they were “economic” — i.e. their marginal cost offer for supply was less than the market price — for half of their minimum operational run-time.

The MSP provided recommendations to the IESO to address the inefficiencies of guarantee programs repeatedly, with it receiving nearly as much attention as CMSCs over the last 20 years.

iii. Legacy Market Lacked a Financially Binding Day-Ahead Market

Similar to the commitment programs for NQS Generators, there was no DAM included in the IAM when it was launched in 2002. The IESO ultimately implemented what became known as the Day-Ahead Commitment Process (“DACP”) in 2006. Nonetheless, the DACP was not financially binding for Market Participants — although NQS Generators could receive a cost guarantee in the DACP — and, as such, did not result in full or efficient participation by many resources.

The IESO concluded that the “failure” of resources to “fully” or “efficiently” participate in the day-ahead commitment process in the legacy market diminished “IESO’s ability to schedule and commit the lowest-cost set of resources to meet the next day’s demand.”[6]

iv. Legacy Market Assumed Fictitious Ramp Rates for Generators

In the legacy market, the market algorithm — which determined hourly and 5-minute market prices — included an assumption that the “ramping” capability of generators was 3-times faster than their actual physical capability (i.e. it assumed they were 3-times “faster” than their real-world performance). This assumption was explicitly included in the market algorithm to suppress price volatility that resulted from the rapid ramping up and down of units. The IESO itself noted that the three-times ramp rate resulted in “price stability” and made it “more likely that slower, less expensive resources will set the price.”[7]

v. Legacy Market Included Low-Priced Emergency (Control Action) Operating Reserve

In the supply stack for Operating Reserve (“OR”), the IESO included an offer to reduce system-wide voltage by 3 per cent and 5 per cent (or other emergency actions), which would theoretically provide hundreds of megawatts of additional OR by reducing demand. This was known as “Control Action Operating Reserve” or CAOR. The primary concern was not the action itself — which is present in other wholesale markets — but rather the price at which it was offered. The IESO added CAOR into the OR stack at a price as low as $30/MW, which meant that in many hours it either suppressed wholesale prices or would create uncertainty in the actual amount of OR available. The IESO included standing supply offers for OR representing voltage reductions of 400 MW for 30-minute OR at $30/MW, and 400 MW for 10-minute OR at $30.10/MW.[8] Another 400 MW was included to represent disregarding the 30-minute OR requirement, with 200 MW priced at $75/MW and 200 MW priced at $100/MW.[9] This amount of fictional OR is significant, considering the IESO would typically schedule between 1,400 MW to 1,600 MW of OR in every hour. This suppressed overall prices both in the OR and energy markets due to co-optimization.

vi. Legacy Market Did Not Properly Value Energy Flowing Across Interties

According to the IESO’s MRP Business Case, under the legacy market, “the price of imports and exports is based on an unconstrained price that at times overvalues or undervalues the energy flowing across the intertie”.[10] The IESO highlighted that, under the legacy market, if the locational marginal price near the intertie was different than the Market Clearing Price (MCP) because of congestion, then the “intertie price calculated will not be accurate and may result in higher costs”.[11] Market Renewal would “correct the pricing at the interties by factoring in the locational marginal price at the intertie in addition to the (Internal Congestion Price)”.[12] Based on analysis conducted between 2015 and 2018, the IESO’s analysis concluded that net exports to MISO and the New York Independent System Operator were 9 per cent and 13 per cent inefficient, respectively.[13] This would amount to $4.60/MWh of costs incurred for MISO net exports and $3.10/MWh for NYISO net exports.[14] The IESO projected that the “inefficiency costs of net exports avoided with improved pricing at the interties” would lead to $28.5 million in savings per year with MRP.[15]

3. THE JUSTIFICATION OF MRP: A FRIEND WITH BENEFITS

Improving the economic efficiency of the IAM is expected to deliver financial benefits to Ontario ratepayers, according to the IESO. The benefits will amount to more than $1 billion in savings over the first ten years of operation (or around $100 million annually, which is less than 1% of the total value of Ontario’s electricity supply costs).[16] These benefits come primarily from the following areas:

-

- More efficient scheduling and commitment of resources in the real-time market will provide $500 million in savings over the first ten years;

- The elimination of “unnecessary” CMSC payments will provide $450 million in savings; and

- The IESO also highlighted that the new market design will reduce the opportunity for “gaming” that resulted in more than $360 million in “clawbacks” in previous years but did not provide a forecasted value of these benefits.

The IESO has also highlighted the benefit of both the “operational certainty” due to the introduction of a financially binding DAM and the value of locational pricing that “could positively impact future investment decisions.”

Overall, market design of MRP broadly aligns with the design of markets across North America, particularly in New York, New England and the mid-western to eastern United States. Many of these markets have been in operation for decades and have incorporated nearly all of the designs included in MRP (apart from the 27-hour Look Ahead Period).

4. REALITY BITES: THE FIRST SIX MONTHS

At the time of writing, the renewed market has been in operation for more than 6 months and there are a number of key observations from a market pricing and dispatch perspective. Importantly, the renewed market has operated through a peak demand season — which typically occurs in the summer months, although extremely cold winters can also test the Ontario grid — and, as such, provides outcomes of the renewed market when the grid is operating on a tight supply/demand balance.

Nonetheless, as with all commentary on highly volatile electricity markets — particularly ones that are just six months old — pricing and dispatch outcomes are expected to evolve over time. As the supply/demand balance evolves — including nuclear refurbishments, new Battery Energy Storage Systems (BESS) and increased system demand — market outcomes will similarly evolve as Market Participants respond to the new market conditions.

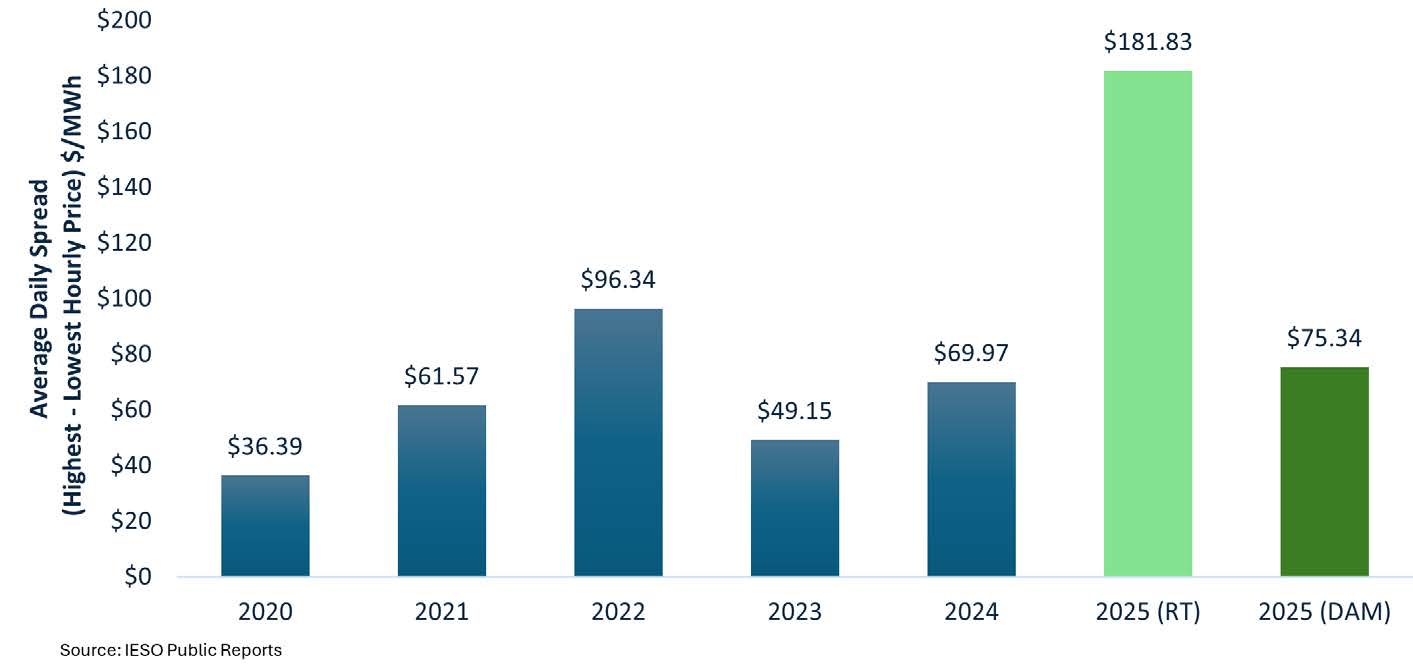

The rollercoaster ride of real-time price volatility

Prices in the real-time market have been significantly more volatile than in the legacy market. The figure below provides the average daily spread between the highest and lowest price hours in the May-to-October timeframe from 2020 to 2025. The average daily spread between the highest and lowest hour real-time price in 2025 was $182/MWh in the first six months of the renewed market — or nearly double the daily spread observed in 2022, the year with the highest spread from 2020 to 2024.[17] It should be noted that 2022 experienced significant volatility in electricity prices due to broader volatility in the commodity markets impacted by the Russian invasion of Ukraine. The daily spread between the highest and lowest price hours in the DAM are higher than four out of the five past years of prices, with 2022 as the exception.

Real-time price volatility under the renewed market is less “impactful” for most load customers, as a majority of generation is purchased in the day-ahead market — with the real-time market largely acting as more of a balancing service for divergences between day-ahead forecasts and real-time conditions on the grid. Any load that is purchased in real-time — by large customers, for example, or by the IESO to address forecast error — is exposed to this volatility. Nonetheless, there are a few underlying factors for the increase in real-time price volatility:

-

- End of the three-times ramp rate – With the fictitious three-times ramp rate assumption removed in the renewed market, the pricing volatility that was previously suppressed is now a feature of real-time pricing outcomes.

- Updated commitment programs – In the legacy market, due to the RT-GCG and DA-PCG commitment programs, multiple units were frequently committed to their minimum physical capability, rather than committing fewer units to their full output capabilities. The “oversupply” for such commitment could put downward pressure on prices and suppress real-time volatility, as there was an abundance of ramping capabilities being committed in many hours. This is discussed in more detail in a later section (see “Commitment Issues”).

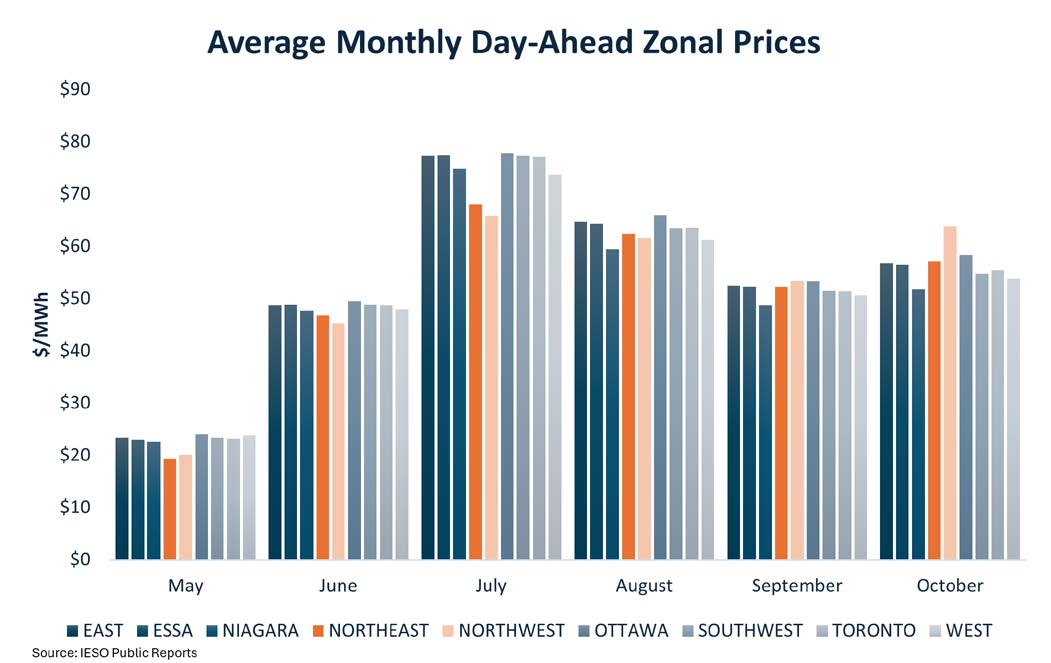

Location, location, location: Price divergence across the IAM

One of the key elements of the renewed market was the introduction of locational prices, or LMPs. LMPs are intended to provide a more accurate price signal, which would, among other features, improve the economic efficiency of the wholesale market by providing a more accurate signal for dispatch, consumption and long-term investment.

Based on historical shadow prices — which were in many ways a proxy for LMPs in the renewed market — the northern zones in the IAM in many hours and months of the year faced structural transmission constraints that limited the amount of supply that could be delivered to the major load centres in southern Ontario. In a market with locational prices, the transmission constraints that limit the amount of low marginal cost supply that could be delivered from northern to southern Ontario would be expected to be reflected in locational prices. The “value” of supply in many hours in northern Ontario would be expected to be less than in most other zones, as there were physical constraints that would limit how much could be delivered. With all loads and suppliers settled on the market price — which did not incorporate the financial impact of transmission losses or congestion — the value of supply or consuming electricity at different points on the grid was not considered.

As hoped for (and as expected), the renewed market has highlighted the locational value of supply based on the physical constraints of the grid. Over the first six months, the average price in the Northwest and Northeast zones was less than nearly all of the other zones in the IAM.[18] In the summer months, the discount was particularly extreme, due to high demand in the southern zones — where most of the load is based — and physical constraints that limited the delivery of supply from the Northeast and Northwest and required dispatch of higher marginal cost resources in the south.

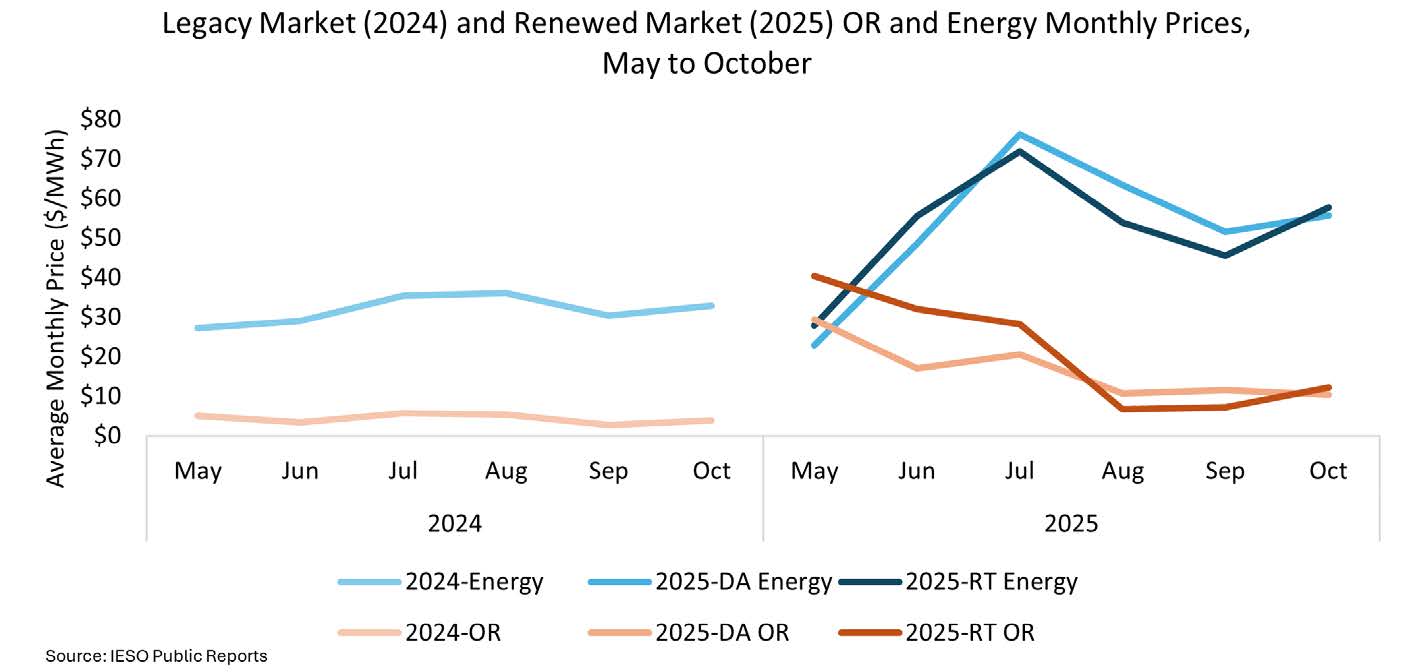

Anything but reserved: OR prices shoot higher

One consistent feature across both the legacy and renewed market is the co-optimization between energy and OR prices. Co-optimization determines the lowest overall cost of providing energy and OR. During times when there is sufficient OR supply, co-optimization has little-to-no impact on the energy price. However, at times when OR supply is facing a shortage, the OR price can put upward pressure on the energy price.

Under MRP, the IESO replaced its policy of including CAOR in the OR supply stack at a price between $30/MW and $100/MW with what is known as an Operating Reserve Demand Curve (ORDC). The ORDC penalty prices are applied when the OR market is tight and includes much higher price laminations compared with CAOR — from $250/MW up to $600/MW (or up to $1,900/MW as a cumulative price) depending on the amount and class of OR that is below the requirement. This new ORDC has meant that there is a new price sensitivity in the market related to the availability of OR that was not present in the legacy market.

In May 2025 when MRP was launched, there happened to be systemic conditions that led to a tight OR supply. Namely, high water levels in various water systems across the province limited the ability of hydroelectric generators to provide OR. This was coupled with fewer fast-ramping dispatchable gas resources online due to shoulder season demand levels and enhanced gas generation unit commitment. This led to a limited availability of OR supply that then triggered higher OR prices and impacted the energy price through co-optimization. In May, 47 per cent of the hours in the DA timeframe had higher or equivalent OR prices compared to the energy price, and 62 per cent of hours in real-time had higher or equivalent OR prices. By June, the OR price more frequently dropped below the energy price, returning to historical patterns more reflective of OR prices acting as an opportunity cost to the energy market. Nonetheless, overall OR prices in the DAM and in RT remain elevated compared to the legacy market.

The monthly average energy and OR prices (10-minute spinning) for the May to October period is shown below for both the legacy market in 2024 and the renewed market in 2025.

Commitment issues: Enhanced commitment in the renewed market

Another key component of the renewed market was the re-design of a number of commitment programs for NQS generators, as well as updates to the dispatch algorithms to include a number of new financial and operational constraints. These updates were intended to more efficiently commit NQS generators and lower overall system costs.

As noted previously, NQS generators are treated differently by the calculation engines and settlement functions than many other resource types, as they have unique financial and operational attributes. Notably, they incur a certain amount of costs to start and maintain operations, as well as physical restrictions on the minimum output and number of hours that they must remain online once they have started.

Under the legacy market, the IESO had designed specific commitment programs for NQS generators to provide a financial guarantee once they are committed and dispatched to address these unique characteristics. But the design of these programs — and their integration into the dispatch algorithm — in the pre-dispatch (i.e. hours prior to real-time) and real-time timeframe did not, according to the IESO, “achieve the most economic commitment of NQS resources.”[19]

-

- First, the commitment programs did not incorporate the total costs of an NQS unit, including its incremental energy costs, start-up costs and what is known as speed-no-load costs. Instead, the units were committed based on their incremental energy offers only — which should broadly reflect their incremental energy costs — and not their total costs. As a result, the IESO could potentially commit resources that appear to be the most economic resource based only on incremental energy offers but may have higher total costs than other units when all of the other costs are considered.

- Second, the pre-dispatch process accounted for each hour separately and did not consider the minimum run time that each unit must remain online once it was committed. This meant that a unit with low incremental energy costs and a very long minimum run-time could be committed instead of a unit with higher incremental energy costs and a much shorter minimum run time. The result is that a higher cost unit could be committed over a competing unit with lower total costs.

The combination of the deficiencies described above could result in economically inefficient commitment of NQS resources, including having multiple high-cost NQS generators committed at the same time running at their minimum loading points — the lowest level of output they can physically operate at — instead of a fewer number of units operating beyond their minimum loading point.

The IESO has stated in multiple forums that the renewed market was intended to address these deficiencies by incorporating what are known as three-part offers — which include all of the unit’s costs — and optimization over multiple hours in both the day-ahead and pre-dispatch algorithms. In short, the updated commitment programs included in MRP were intended to “improve the efficiency” of commitment.

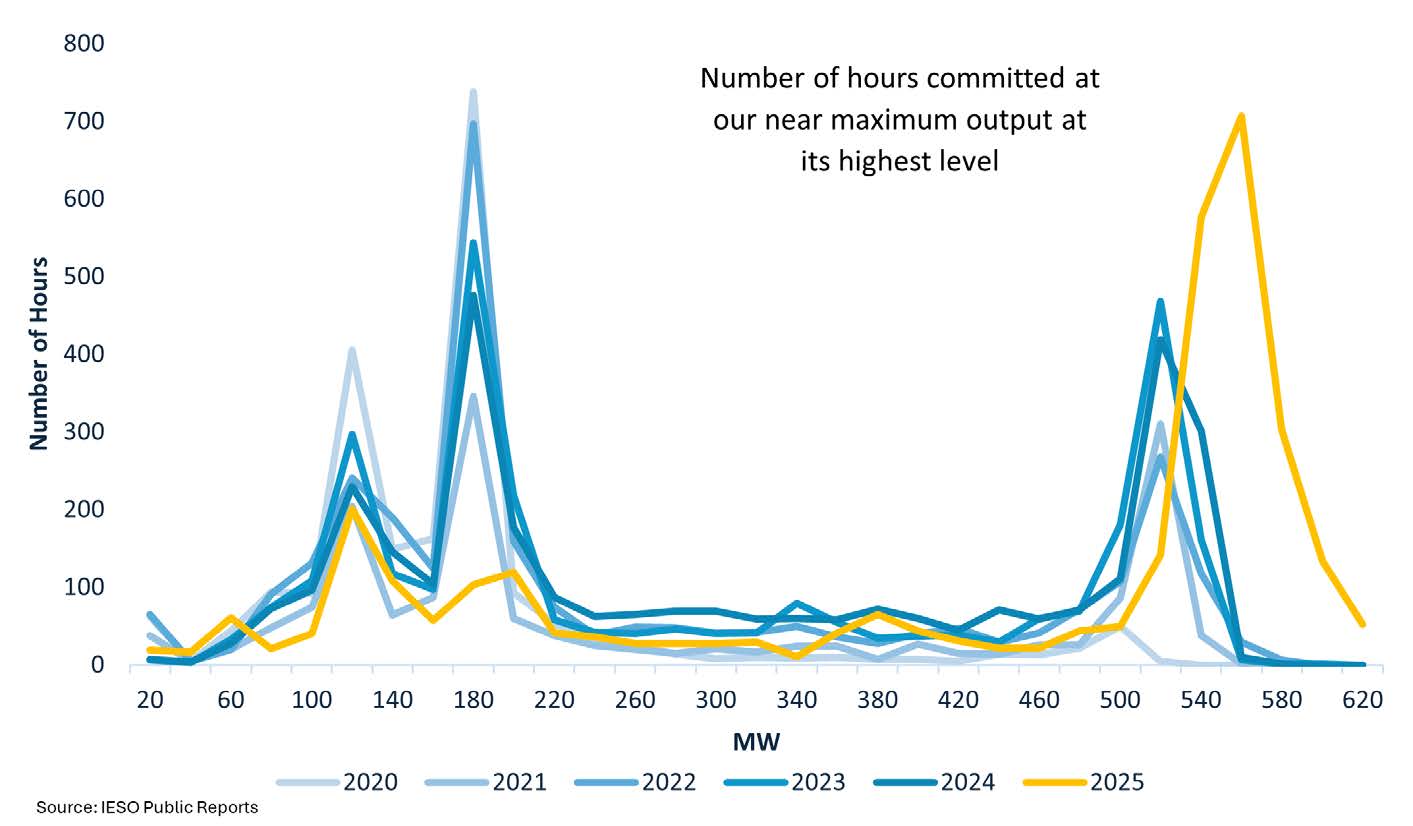

One way to test whether the efficiency of commitment has been improved in the renewed market is to compare the number of hours in the renewed versus legacy market when an NQS generator operated at its minimum operating point compared to a higher output. By committing units on a more holistic basis — incorporating all of their costs and physical commitments — we would expect that once a unit is committed it would operate at a higher capacity factor, as opposed to operating at its minimum allowed output without considering commitment of other units. Overall, the number of hours when a unit is operating at its minimum loading point should decline in the renewed market (all else being equal).

The following graph highlights the number of hours when the combustion turbines at a large, combined cycle gas turbine facility operated at different output levels in the first six months of the renewed market compared to the same months in previous years. As can be seen, the number of hours where the unit operated at or near its minimum level decreased materially under the renewed market, while the hours where it operated at or near its maximum output level increased. While this analysis is simplified, it highlights that the stated intention of updating the commitment processes — to ensure that units were more efficiently committed — appears to have occurred. Committing a unit more efficiently — by dispatching more supply rather than incurring start-up costs for multiple units, for example — could result in lower overall costs for ratepayers, one of the intended outcomes of the renewed market.

5. DOCTOR, DOCTOR: POTENTIAL EARLY ISSUES WITH MRP IMPLEMENTATION

While the overall implementation of the renewed market has been smooth from a grid-wide perspective (i.e. it did not require a roll-back or other extreme intervention), it has resulted in both unintended (or unexpected) outcomes and the need to update certain Market Rules and specific components of the calculation engines. As of January 2026, the Market Surveillance Panel (“MSP”) that is tasked with monitoring and investigating design flaws in the IESO wholesale market has not provided any commentary on the first six months of the renewed market.

Notably, the IESO has repeatedly highlighted what it has called a “defect” that resulted in rapid changes in its demand calculation by hundreds of megawatts and required a “workaround” and administrative pricing.

The IESO first highlighted concerns around demand fluctuations in an August presentation to stakeholders but stated that given the “unpredictable nature” of many of the variables used to calculate demand, there can be “significant changes in demand from one interval to the next attributed to one or many different variables.” The IESO did note that “tool or software defects or failures can occasionally result in erroneous spikes in demand.”[20]

The IESO in its 6-month review of the renewed market to stakeholders in November stated that there was a “defect causing demand fluctuations.”[21] The IESO concluded that the calculation engine was overstating demand by including Hourly Demand Response (“HDR”) resources when they were placed on standby. The IESO introduced a “work around” to mitigate the defect. In total, there were 38 intervals where the “workaround” did not mitigate the impact of the defect and prices needed to be administered by the IESO.

The IESO has also highlighted a number of “specific and limited” instances where “inappropriate” out-of-market payments were made to Market Participants. To address these payments, the IESO has proposed a number of changes to the Market Rules.

Another issue that has not yet been highlighted by the IESO is the increased dispatch interventions that have occurred since the launch of Market Renewal. According to the IESO, the Dispatch Deviation Report is “an after-the-fact summary of the number of occurrences where the IESO has taken an action that deviates from the results of the dispatch algorithm and does not impact dispatching or market settlements”.[22] The report is important, as it is meant to highlight the number of interventions by the IESO. The actions taken by the IESO are either a one-time dispatch or a blocked dispatch to resources for system reliability purposes, with blocked dispatches occurring far more frequently than one-time dispatches.

When comparing the interventions by the IESO since the launch of Market Renewal with the monthly interventions under the legacy market, the number of interventions under the renewed market is notably higher. For example, in July 2025, there were 14,929 blocked and one-time dispatches for the month, averaging 1.7 IESO interventions to the dispatch algorithm every 5 minutes (noting 5-minute intervals can experience multiple interventions). Compared to July 2024, July 2025 has recorded more than triple the number of blocked and/or one-time dispatches.[23]

6. CLOSING TIME: CONCLUDING REMARKS ABOUT THE FIRST SIX MONTHS OF THE RENEWED MARKET

The IESO has successfully crossed over into the renewed market. Whereas prices in the legacy market were suppressed due to the number of design features, a transparent price that incorporates congestion and other factors is now in place due to the design features introduced as part of MRP. Overall, prices have been higher in the renewed market compared to historical averages.

High prices are not necessarily a bad outcome if they more accurately reflect the cost of supply and consumption. High market prices can also be the result of higher gas (and carbon) prices, or increased demand — both of which have occurred in the first six months of MRP. However, when these effects are removed, prices experienced in the renewed market remain higher than in the legacy market. In the long-run, more accurate pricing should improve the overall efficiency of the market and, subsequently, reduce the long-term costs to ratepayers. But there are many different policy decisions that can be made that may blunt this signal over time.

Ontario is facing a much tighter supply/demand balance over the next decade — certainly one that is in stark contrast to the prevalence of Surplus Baseload Generation (SBG) that Ontario experienced over the last decade. The impact of the design features of MRP are just one component of future electricity prices and dispatch. Nonetheless, a number of the “band-aids” that blunted the price signal in the legacy market have been removed at the same time that the grid is becoming increasingly “tight”, and prices are expected to move higher while remaining volatile. Data available since the launch of MRP has already provided some insights into pricing in the renewed market, but significant uncertainty remains regarding the impact of Ontario’s changing supply/demand balance, including a significant resurgence in Ontario’s nuclear fleet and the rapid rise in data centre demand, among other factors. The upcoming years of tight supply conditions may lead to amplified price impacts that are independent of the renewed market design.

-

* Brady Yauch is the Director of Markets and Regulatory at Power Advisory. While at Power Advisory he has provided extensive advice to a range of clients regarding wholesale market prices and wholesale market design across Canada and the United States. Prior to Power Advisory he worked at the Market Assessment Unit (MAU) supporting the Market Surveillance Panel. He has a Masters in Economics from York University and Masters in Cultural Politics from the University of Edinburgh.

Brendan Callery is the Senior Manager of Eastern Canada at Power Advisory LLC. Since the launch of Market Renewal in Ontario, Brendan has been analyzing market outcomes with Brady Yauch and the Power Advisory team, contributing to the Power Advisory market update newsletters, presenting the material in public webinars and advising clients. Prior to joining Power Advisory in 2022, Brendan worked at the IESO and Ontario Power Authority for 9 years, including 3 years supporting the OEB’s Market Surveillance Panel in the Market Assessment Unit of the Market Assessment and Compliance Division (MACD). He has a Bachelor of Applied Science in Civil Engineering from Queen’s University.

[1] See Ontario Energy Board, Congestion Payments in Ontario’s Wholesale Electricity Market: An Argument for Market Reform, Market Surveillance Panel (Ontario Energy Board, 2016), online (pdf): <oeb.ca/oeb/_Documents/MSP/MSP_CMSC_Report_201612.pdf>; See also Ontario Energy Board, Congestion Payments in Ontario’s Wholesale Electricity Market: An Argument for Market Reform, Market Surveillance Panel (Ontario Energy Board, 2016), online (pdf): <oeb.ca/oeb/_Documents/MSP/MSP_CMSC_Report_201612.pdf>; See also IESO Market Rule Description Evidence in Response to Procedural Order No. 2 (2024), EB-2024-0331, online (pdf): Independent Electricity System Operator <rds.oeb.ca/CMWebDrawer/Record/875538/File/document> [IESO Market Rule Description Evidence].

-

[2] See Independent Electricity System Operator, Market Renewal Program: Energy Stream Business Case, BC-165 (Ontario: Independent Electricity System Operator, 2019), online (pdf): <ieso.ca/-/media/Files/IESO/Document-Library/market-renewal/MRP-Energy-Stream-Business-Case-2019.pdf>.

-

[3] Ibid.

-

[4] See the 2016 report and multiple MSP reports among multiple other examples. Inefficient CMSC payments were discussed at length in nearly every MSP report: Ontario Energy Board, Monitoring Report on the IESO-Administered Electricity Markets, Market Surveillance Panel (Ontario Energy Board, 2014), online (pdf): <oeb.ca/oeb/_Documents/MSP/MSP_Report_Nov2012-Apr2013_20140106.pdf>; See also Ontario Energy Board, Monitoring Report on the IESO-Administered Electricity Markets, Market Surveillance Panel (Ontario Energy Board, 2011), online (pdf): <oeb.ca/oeb/_Documents/MSP/MSP_Report_20110310.pdf>.

-

[5] See IESO Market Rule Description Evidence, supra note 1, IESO’s filing as part of the Market Rule appeal by a group of NQS generators.

-

[6] Ibid.

-

[7] Ibid.

-

[8] See Independent Electricity System Operator, Market Manual 7: System Operations, Part 7.2, online (pdf): <ieso.ca/-/media/files/ieso/document-library/market-rules-and-manuals-library/market-manuals/system-operations/so-neartermassessreport.pdf>.

-

[9] Ibid.

-

[10] See supra note 2.

-

[11] Ibid.

-

[12] Ibid.

-

[13] Ibid.

-

[14] Ibid.

-

[15] Ibid.

-

[16] These values and quotes from the IESO’s 2019 Benefits Case for MRP. See Independent Electricity System Operator, Market Renewal Program: Energy Stream Business Case, BC-165 (Ontario: Independent Electricity System Operator, 2019), online: <ieso.ca/-/media/Files/IESO/Document-Library/market-renewal/MRP-Energy-Stream-Business-Case-2019.pdf>.

-

[17] Note that all data in the following graphs comes from publicly available IESO data, which can be found here: Independent Electricity System Operator, “Report: Public” (last visited 30 January 2026), online: <reports-public.ieso.ca/public>.

-

[18] The Niagara zone is the one zone in southern Ontario that has experienced structurally lower prices than the load-weighted average Ontario Zonal Price (“OZP”).

-

[19] See IESO’s NQS evidence, IESO Market Rule Description Evidence, supra note 1.

-

[20] See the IESO’s August presentation to stakeholders: Independent Electricity System Operator, “Update on Renewed Market Performance and Operations” (21 August 2025), online (pdf): <ieso.ca/-/media/Files/IESO/Document-Library/engage/renewed-market/rmo-20250821-presentation-renewed-market-update.pdf>.

-

[21] See the IESO’s November presentation: Independent Electricity System Operator, “Updtae on Renewed Market Performance and Operations” (26 November 2025), online (pdf): <ieso.ca/-/media/Files/IESO/Document-Library/engage/renewed-market/rmo-20251126-presentation-renewed-market-update.pdf>.

-

[22] See the Independent Electricity System Operator, “News and Updates: Change to Dispatch Deviation Report” Updtae on Renewed Market Performance and Operations” (10 February 2022), online: <ieso.ca/en/Sector-Participants/IESO-News/2022/02/Change-to-Dispatch-Deviation-Report>.

The Dispatch Deviation Report can be found on the IESO’s Public Reports page: Independent Electricity System Operator, “Dispatch Deviation” (last visited 30 January 2026), online: <reports-public.ieso.ca/public/DispDeviation>.

-

[23] See the July 2025 Dispatch Deviation Report (14,929 blocked and one-time dispatches from the IESO): Independent Electricity System Operator, “Dispatch Deviation Report – July 2025” (last visited 30 January 2026), online: <reports-public.ieso.ca/public/DispDeviation/PUB_DispDeviation_202507.html>.

See also the July 2024 Dispatch Deviation Report (4,366 blocked and one-time dispatches from the IESO): Independent Electricity System Operator, “Dispatch Deviation Report – July 2024” (last visited 30 January 2026), online: <reports-public.ieso.ca/public/DispDeviation/PUB_DispDeviation_202407.html>.