1. INTRODUCTION

The Rate of Last Resort (“RoLR”), is Alberta’s current default electricity rate, meaning it is available to all small retail electricity consumers who cannot or will not sign a contract with a competitive retailer.[2] RoLR rates offered by regulated providers are fixed for two-year terms, and they can be adjusted within a 20 per cent bandwidth upon renewal.[3] The establishment of the Rate of Last Resort Regulation appears to have been intended to correct the price volatility experienced under the province’s previous default rate, the Regulated Rate Option, which fluctuated monthly to reflect relevant forward market prices.[4] With many competitive retailers offering various fixed-rate and variable-rate contracts, the Rate of Last Resort provides price stability to individuals for whom competitive fixed-rate contracts are unavailable.

Low-income households are those who are the most vulnerable to variable electricity rates. These consumers tend to spend a relatively large proportion of their income on energy,[5] meaning they risk falling behind on their electricity payments if their bills turn out to be higher than expected. Yet, since low-income customers tend to have low credit scores, they are often ineligible for fixed-rate contracts offered by competitive retailers.[6] As such, the only competitive rates available to these consumers are those offered through variable-rate contracts, implying many low-income consumers may elect the RoLR to avoid price uncertainty. Indeed, since 80 per cent of residential consumers were on competitive contracts as of the end of 2025,[7] it seems as though nearly all eligible contract consumers have made the switch off of the default rate.

However, the stability of the RoLR eliminates price risk for small retail consumers only. Since regulated providers must purchase generation to serve their customers, they are exposed to the price variability inherent in Alberta’s competitive electricity market. Moreover, since the Rate of Last Resort is available to all residential consumers, regulated providers cannot discourage customers from using the RoLR when their costs of electricity increase. Considering that the rates offered by competitive retailers incorporate prevailing pool prices,[8] consumers who are eligible for contracts tend to search for alternative rates and providers when market prices rise suddenly.[9] Therefore, there is a strong incentive for high-income consumers to switch to the RoLR when pool prices rise, as the RoLR cannot adjust when market prices move. The ability to switch by consumers on contracts is enabled by the fact that cancelling a competitive contract prior to the end of its term is typically inexpensive.[10] As such, RoLR providers must account for the risk that consumers coming to the end of their fixed-rate contract or on a variable-rate contract may switch over to the RoLR if pool prices spike. The only way to control this risk is for RoLR providers to set a relatively high price.

This paper considers whether the risk of migration by high-income consumers to the RoLR corresponds to low-income consumers paying higher RoLR rates than should be necessary? To answer this question, I developed a model to illustrate the differences in RoLR rates when (1) only non-contract consumers are permitted to use the RoLR (termed the ‘fair’ scenario), and (2) when switching to the RoLR by contract consumers is allowed (termed the ‘break even’ scenario). Details of the model are presented in the appendix. The model shows that when expected volatility of electricity prices increases, RoLR providers are forced to increase the RoLR price substantially in order to avoid switching into the RoLR. The validity of this model is then supported by a comparative analysis of constructed fair and break-even RoLR rates for each two-year period from 2012 to 2024, with factors heightening the risk of switching listed thereafter.

2. COMPARATIVE ANALYSIS OF CONSTRUCTED ROLR RATES

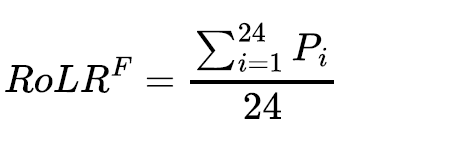

In this section, I compare fair RoLR rates in the absence of consumer switching to the rates which would allow RoLR providers to break even when switching to the RoLR could occur. Since future prices are unknown, I illustrate how the fair and break-even RoLR prices would have compared for each two-year period between 2012 and 2024 using historical data on pool prices[11] and on the proportion of consumers on competitive contracts.[12] Obviously, the break-even rates constructed for the purposes of this analysis were not observed since the RoLR regulation did not come into effect until the beginning of 2025.

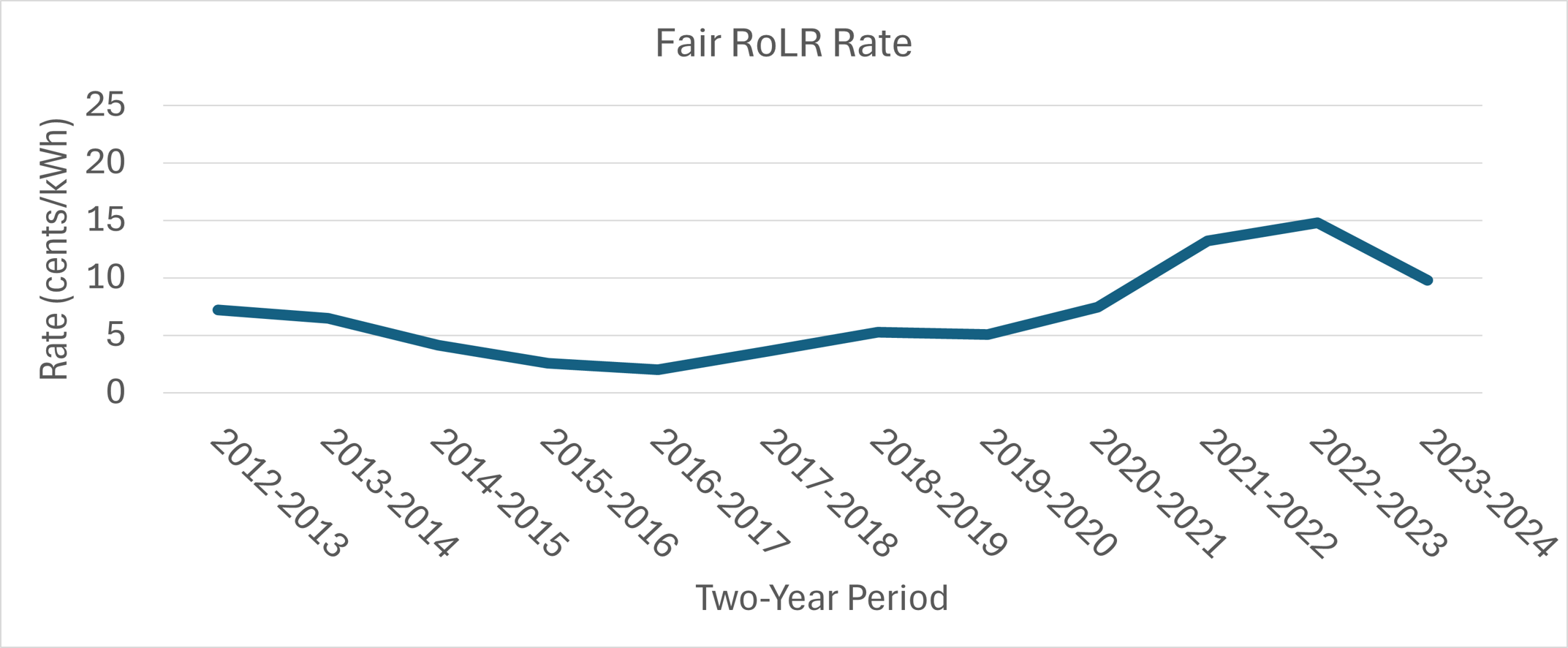

i. Fair RoLR Rates

Figure 1 plots the rates which would allow RoLR providers to just break even when only non-contract customers utilize the RoLR.

ii. Comparing the Fair RoLR Rates to the Break-Even RoLR Rates

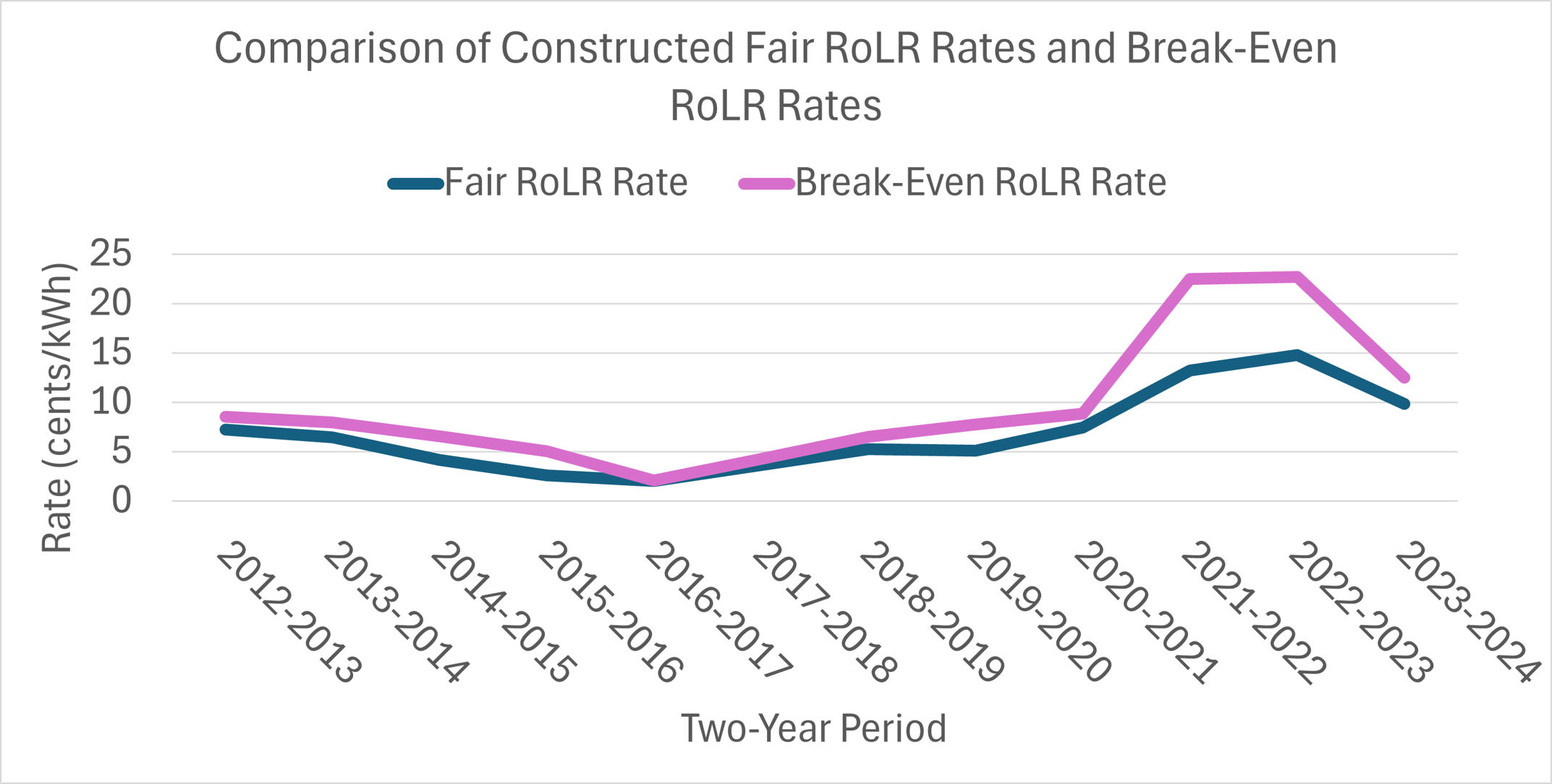

In Figure 2, the fair RoLR rates are plotted against the rates which would let regulated providers break even when a proportion of contract consumers switch to the RoLR in the month with the highest average pool price.

Evidently, the rates necessary to recover RoLR-related costs when consumer switching is permitted are higher than the rates which would prevail if the RoLR were only utilized by a stable group of consumers. As the RoLR cannot be changed to account for minor or infrequent pool price changes,[13] break-even RoLR rates must account for sizeable influxes of customers when pool prices increase. Indeed, this comparison illustrates that non-contract consumers subsidize the ability of contract consumers to migrate to the RoLR by paying higher-than-necessary rates in return for price certainty.

iii. Factors which Impact the Markup on Break-Even RoLR Rates Relative to Fair RoLR Rates

It is clear from Figure 2 that the differences between fair and break-even RoLR rates are not uniform across time periods. There are some periods where fair and break-even rates are almost indistinguishable, while in others the break-even rates are several cents/kWh higher than their fair-rate counterparts. The magnitude of the differences between fair and break-even RoLR rates can be explained by (1) the variability in monthly average pool prices and (2) the proportion of contract consumers during the month of switching.

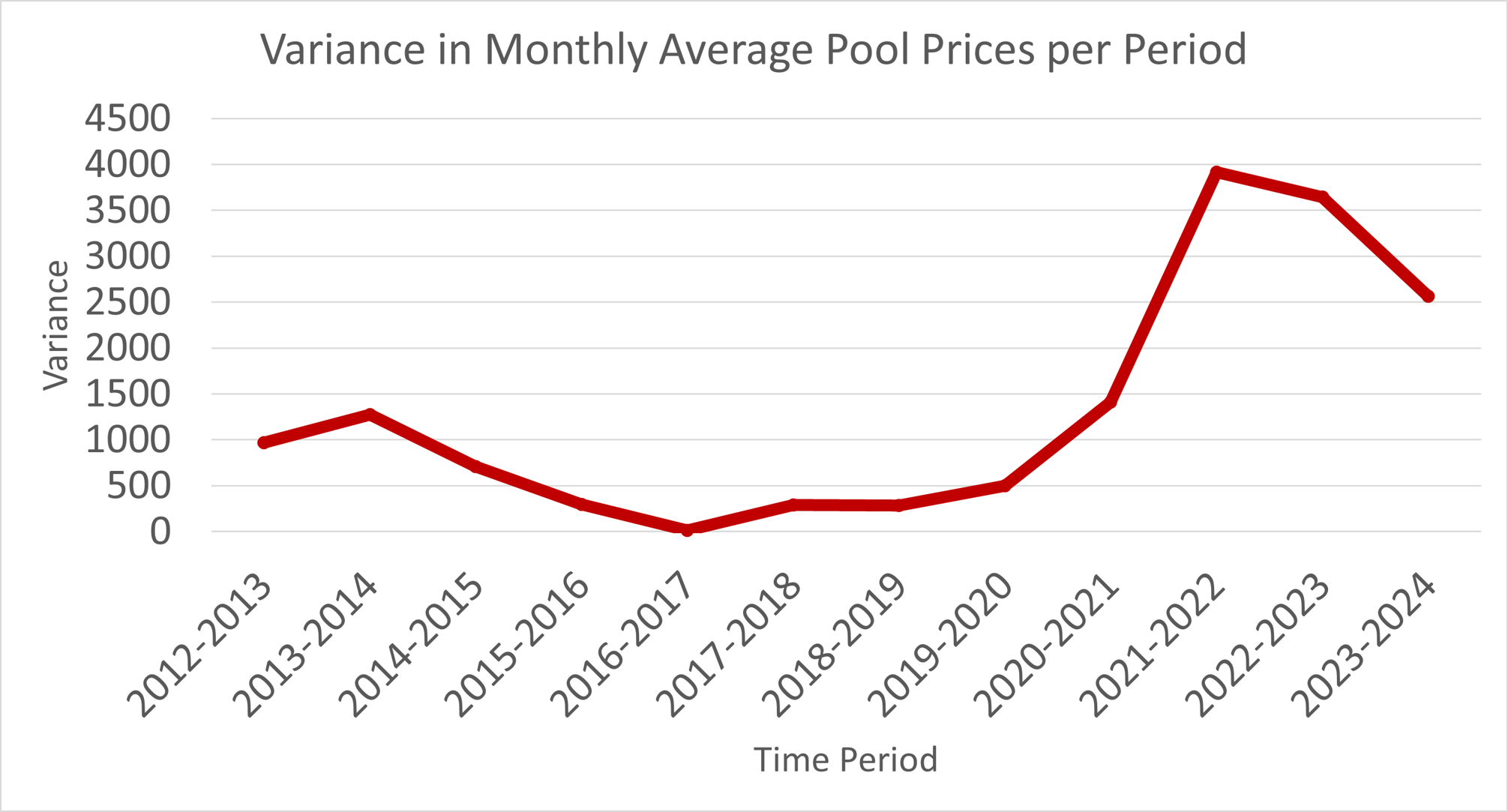

Variance in Monthly Average Pool Prices from 2012 to 2024

Figure 3 shows the variance in monthly average pool prices in each two-year term from 2012 to 2024. Years with greater pool price volatility see higher variances in monthly average pool prices.

The trend in the variance of monthly average pool prices mimics the fluctuations in the differences between break-even and fair RoLR rates. Indeed, recall that, in the previous figure, the gap between break-even and fair RoLR rates began to close leading up to the 2016-2017 period, with these rates being almost identical as monthly average pool price variance reached its minimum. Yet, as monthly average pool prices began to vary more, the gap between these rates started to reopen, with the largest discrepancy being in the 2021-2022 period. Incidentally, this period experienced the highest variance in monthly average pool prices relative to the other periods under consideration.

These results indicate that larger variances in monthly average pool prices correspond to notable increases in break-even RoLR rates relative to fair RoLR rates. This makes sense intuitively; the larger the variance in monthly average pool prices, the larger the difference between the average pool price in the month of switching and the average pool prices in the months prior, corresponding to a greater volume of contract consumers that will be incentivized to switch to the RoLR. Additionally, greater variability in monthly average pool prices implies shorter durations of sustained price spikes, meaning the increase in expected average costs incurred by providers in the break-even scenario will be more sudden and severe relative to years with lower variances.

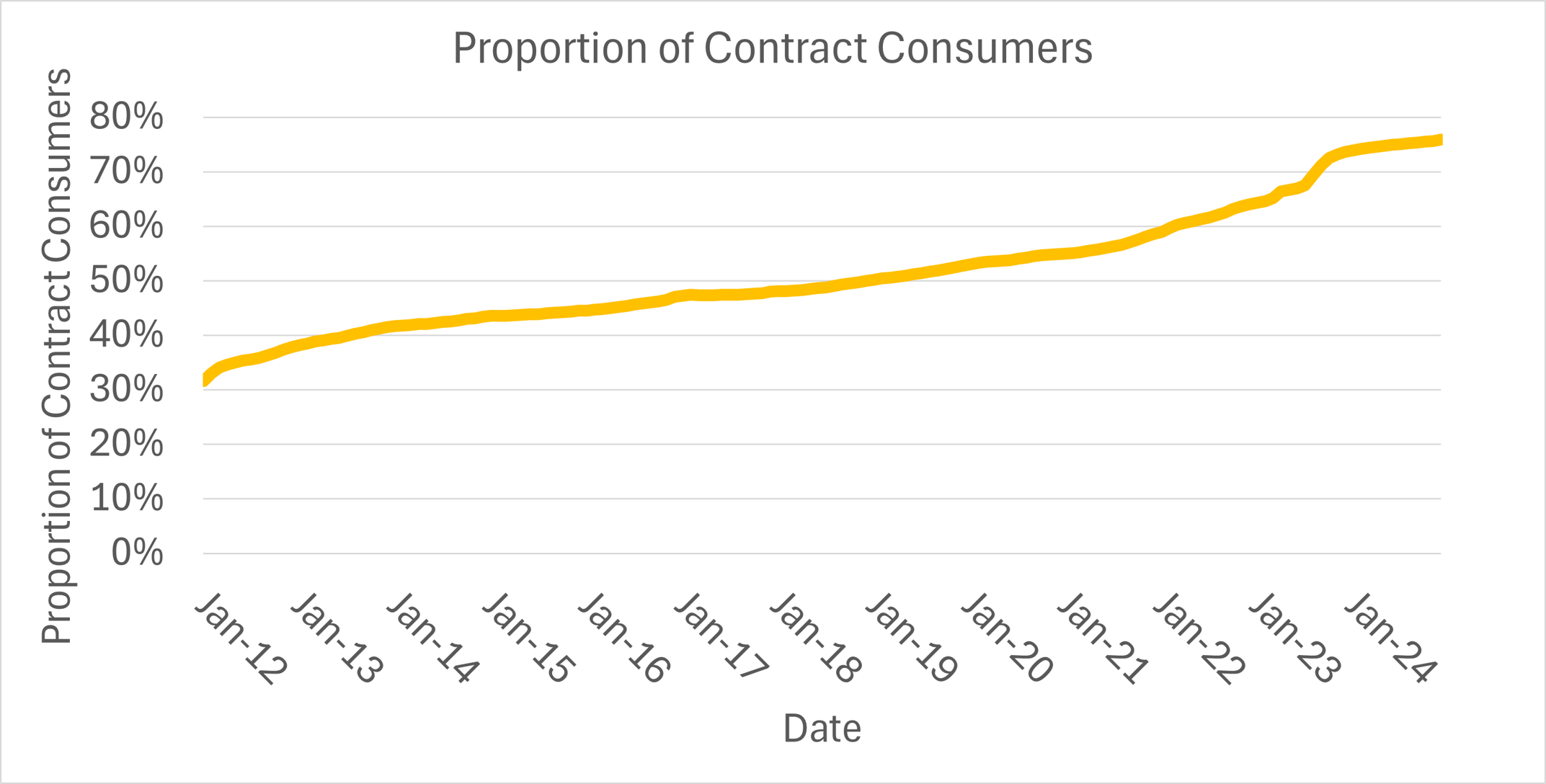

Proportion of Contract Consumers from 2012 to 2024

Figure 4 shows the proportion of residential consumers on competitive fixed-rate and variable-rate electricity contracts for each month spanning 2012 to 2024.

Clearly, there has been a steady increase in the proportion of consumers on contracts from January 2012 to December 2024. This is important, since the risk of switching becomes more tangible when there is a larger proportion of consumers on contracts. The extent of consumer switching, however, depends on the barriers individuals face when they attempt to cancel a contract. Though all contracts have a mandatory 10-day cooling off period, where consumers can cancel contracts immediately without financial penalty,[14] cancellations made after this period typically require 10 to 90 days’ notice, with some retailers charging early exit fees as penalties.[15] These frictions insulate RoLR providers from extensive switching when pool prices rise substantially, since consumers with more scrutinizing cancellation policies have less to gain from moving to the RoLR. Yet, these cancellation policies do not disincentivize switching to the RoLR entirely; consumers with lenient contracts incur relatively low switching costs, meaning migration to the RoLR is quite easy. So, while the risk of switching, and thus burden on non-contract consumers, would be higher in the absence of exit fees and required cancellation notices, switching is still advantageous for some contract consumers. Coupled with the fact that more contract consumers entail more contract expirations in months with high pool prices, RoLR providers face greater price risk when many consumers are on fixed-rate and variable-rate competitive plans.

3. CONCLUSION

The introduction of the Rate of Last Resort Regulation in January 2025 provided a two-year fixed default electricity rate to small retail electricity consumers in Alberta. In contrast to its variable-rate predecessor, the Regulated Rate Option, the RoLR ensures a stable price for consumers, which may be particularly important for low-income households. However, because the RoLR price is fixed in advance for 2 years at a time, the RoLR is a valuable option to contract consumers, who can switch to it if pool prices increase. Contract consumers do not pay for this option: it is non-contract consumers who bear the implicit option premium, through elevated prices on the RoLR.

Since non-contract consumers tend to be relatively low-income, lacking secure employment that would enable them to obtain lower-priced contracts for their household electricity,[16] the implication of the analysis in this paper is that low-income households in Alberta are subsidizing the electricity consumption of wealthier consumers in the province, by paying above their own costs of electricity, by subscribing to the RoLR. While the size of the subsidy depends on the willingness and ability of other consumers to switch over to the RoLR opportunistically, as well as the volatility of pool prices, the analysis using 2012-2024 data suggests that the excess costs may be quite substantial, with non-contract consumers typically paying at least 10 per cent above the fair price, and sometimes much more. The cost of price stability, given the design of the RoLR, is a substantial transfer from the poorest households in the province to those with greater financial capability.

This suggests that the RoLR should be modified. For example, shortening the RoLR to a one-year fixed price would substantially reduce the need for providers to charge above costs. Alternatively, the RoLR could be set on a rolling two-year period to incorporate changes in current and forecasted pool prices, giving contract consumers less of an incentive to switch when the cost of energy rises. Even allowing the RoLR to adjust every so often to account for changes in market conditions, like what is seen with Maryland’s default electricity rate[17], would significantly relieve the pressure consumer migration places on RoLR providers’ expected average costs.

APPENDIX 1: THE MATHEMATICAL FORMULATION OF THE MODEL

Model Assumptions

For the purposes of this analysis, I have assumed that the sole costs RoLR providers incur arise from the procurement of generation through Alberta’s power pool. Any costs associated with transmission, distribution, and billing are excluded from the model, as these costs are not included in the energy charges faced by consumers.[18] While RoLR providers may also purchase some or all of their generation through forward contracts, there is no specific method of generation procurement required under the Rate of Last Resort Regulation.[19] Additionally, since the rates offered through competitive contracts are based largely on pool prices (as acknowledged previously), the risk of switching by contract consumers does not arise from fluctuating forward prices. This indicates pool prices better reflect the increase in costs experienced by RoLR providers when consumer migration is of concern.

Additionally, in the break-even scenario, I have assumed that contract consumers only switch to the RoLR in the month with the highest average pool price, where the willingness to switch follows a uniform distribution based on the savings the RoLR offers relative to that month’s average pool price. These assumptions allow the model to account for consumer migration that follows from pool price variability, but they eliminate the noise and potential error that can stem from more granular estimates of consumer switching rates. Furthermore, we would not expect to see additional switching to the RoLR following the month with the highest average pool price, as the savings in these months would not be as substantial as if these consumers had switched earlier.

Derivation of the Fair RoLR Rate

Let α be the proportion of contract consumers in a given two-year period. This implies that the proportion of non-contract consumers in said two-year period is given by 1 – α. Furthermore, let Pi, i = 1, 2, …, 24, be the average pool price in month i.

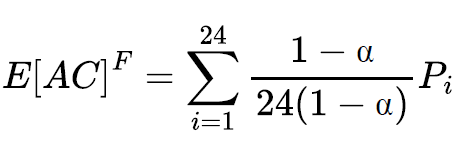

In the fair scenario, RoLR providers serve 1 – α consumers in each month for which their RoLR rates are in place. This implies that, for the duration of a RoLR term, a total of 24(1 – α) consumers are served. Since the average price of generation in a month is given by that month’s average pool price, the expected average cost associated with the provision of the RoLR is given by

which simplifies to

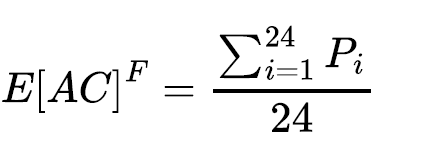

So, the RoLR rates necessary for providers to break even in this scenario are given by

Derivation of the Break-Even RoLR Rate

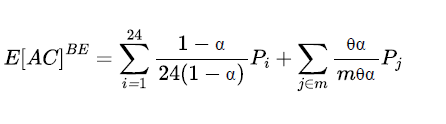

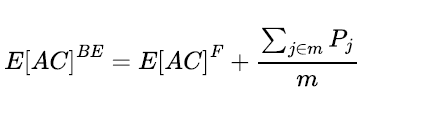

Now, when consumer migration is allowed, RoLR providers serve non-contract customers for every month their RoLR rates are in place, and they serve a proportion of contract consumers in months with comparably high average pool prices. Let θ represent the proportion of contract consumers who switch to the RoLR in the month with the highest average pool price. Furthermore, let m represent the number of months RoLR providers serve contract customers. This means that, for each of the m months, RoLR providers serve θα contract consumers, so mθα contract consumers are served in total. The expected average cost associated with providing the RoLR is this circumstance is given by

which simplifies to

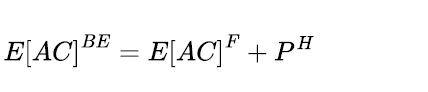

or

where PH gives the average pool price over the months where contract consumers are on the RoLR.

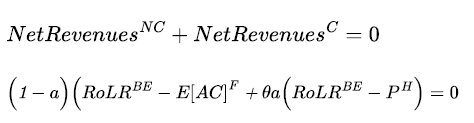

Now, in the break-even scenario, the net revenues RoLR providers receive from serving non-contract consumers are given by

![]()

Likewise, the net revenues RoLR providers receive from serving θα contract consumers are given by

![]()

As such, the break-even RoLR rate, RoLRBE, occurs when

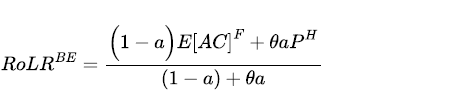

which simplifies to

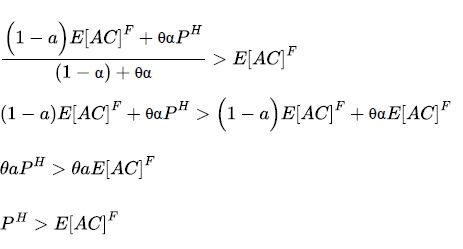

To determine when the break-even RoLR rate is greater than the fair RoLR rate, we want to find the conditions for which

![]()

We have

Recall that E[AC]F is the average of the monthly average pool prices prevailing over the RoLR’s 2-year term and PH is the average of the monthly average pool prices that warrant utilization of the RoLR by contract consumers. Since PH gives greater weight to high monthly average pool prices, it is apparent that E[AC]F will never be higher than PH, meaning the RoLR rates necessary for providers to break even when consumer switching is allowed will always be above the sufficient RoLR rates in the fair scenario.

APPENDIX 2: A NOTE ON THE ESTIMATION OF THETA

The calculation of θ is recursive in nature: its measurement depends on the magnitude of savings the RoLR offers, but the computation of the break-even RoLR rate depends on θ itself. To work around this complication, θ was estimated to be the percentage change in the average pool price from the months prior to contract consumer switching and the month in which consumer switching was to take place. This adaptation ensures θ measures the willingness to switch after contract consumers have faced some significant price change.

-

* I appreciate the guidance of Dr. Aidan Hollis in developing this paper but note that any remaining errors are my own. I acknowledge the financial support of the Dr. Albert Herman Award in Economics.

1 Disclaimer: the author of this article is currently employed with the Alberta Utilities Commission as a summer student. However, this paper was completed in its entirety prior to the start of that employment, and the views and opinions expressed herein are solely those of the author and do not reflect the official policy or position of the Alberta Utilities Commission.

-

2 Alberta Utilities Commission, “History of the Electricity Industry” (last visited 4 January 2026), online: <auc.ab.ca/history-electric-industry>.

-

3 Rate of Last Resort Regulation, Alta Reg 262/2005, s 11(4).

-

4 Market Surveillance Administrator (Alberta), Alberta Retail Markets for Electricity and Natural Gas: A Description of Basic Structural Features (17 July 2014).

-

5 KP Green et al, Energy Costs and Canadian Households: How Much Are We Spending? (Vancouver: Fraser Institute, 2016) at 18–19.

-

6 J McIlroy & B Agar, Affordable Home Energy for All: How Alberta Can Help Its Most Vulnerable Households Escape Energy Poverty (Calgary: Pembina Institute, 2025) at 5.

-

7 Market Surveillance Administrator (Alberta), “Retail Statistics” (last visited 9 April 2026), online: <albertamsa.ca/documents/retail-and-rate-cap/retail-statistics>.

-

8 Kristjana Kellgren, interview by Chloe Haley (20 February 2025) [unpublished, conducted via Microsoft Teams].

-

9 Yiang Guo, Derek EH Olmstead & Andrew H Wilkins, “What Drives Consumers to Switch Retailers? Evidence from the Alberta Electricity Market” (2025) 206 Energy Pol’y 114770 at 1, 2, 9.

-

10 Utilities Consumer Advocate, “Cost Comparison Tool” (last visited 4 January 2026), online: <ucahelps.alberta.ca/cost-comparison-tool/%E2%80%BA>.

-

11 Alberta Electric System Operator, “Daily Average Price” (last visited 11 September 2025), online: <ets.aeso.ca>.

-

12 Supra note 7.

-

13 Supra note 3 at s 11(3).

-

14 Consumer Protection Act, RSA 2000, c C-26.3, s 27.

-

15 Utilities Consumer Advocate, “How to Switch Energy Retailers” (last visited 9 April 2026), online: <ucahelps.alberta.ca/residential/electricity/how-to-switch-energy-retailers>.

-

16 Cindy Tran, “’Rate of Last Resort’ Will Make Alberta Electricity Rates Less Volatile but More Expensive in the Long-Haul, Experts Say”, Edmonton Journal (19 January 2025), online: <edmontonjournal.com/news/local-news/rate-of-last-resort-will-make-alberta-electricity-rates-less-volatile-but-more-expensive-in-the-long-haul-experts-say>.

-

17 Office of People’s Counsel, State of Maryland, “Electric SOS Pricing” (last visited 8 April 2026), online: <opc.maryland.gov/Consumer-Learning/Electricity/Utility-Standard-Offer-Service-Rates>.

-

18 Utilities Consumer Advocate, “Understanding Your Bill” (last visited 4 January 2026), online: <ucahelps.alberta.ca/residential/electricity/understanding-your-bill>.

-

19 Supra note 3 at s 11(1).